Understanding Portfolio Management Services (PMS) in India

Introduction

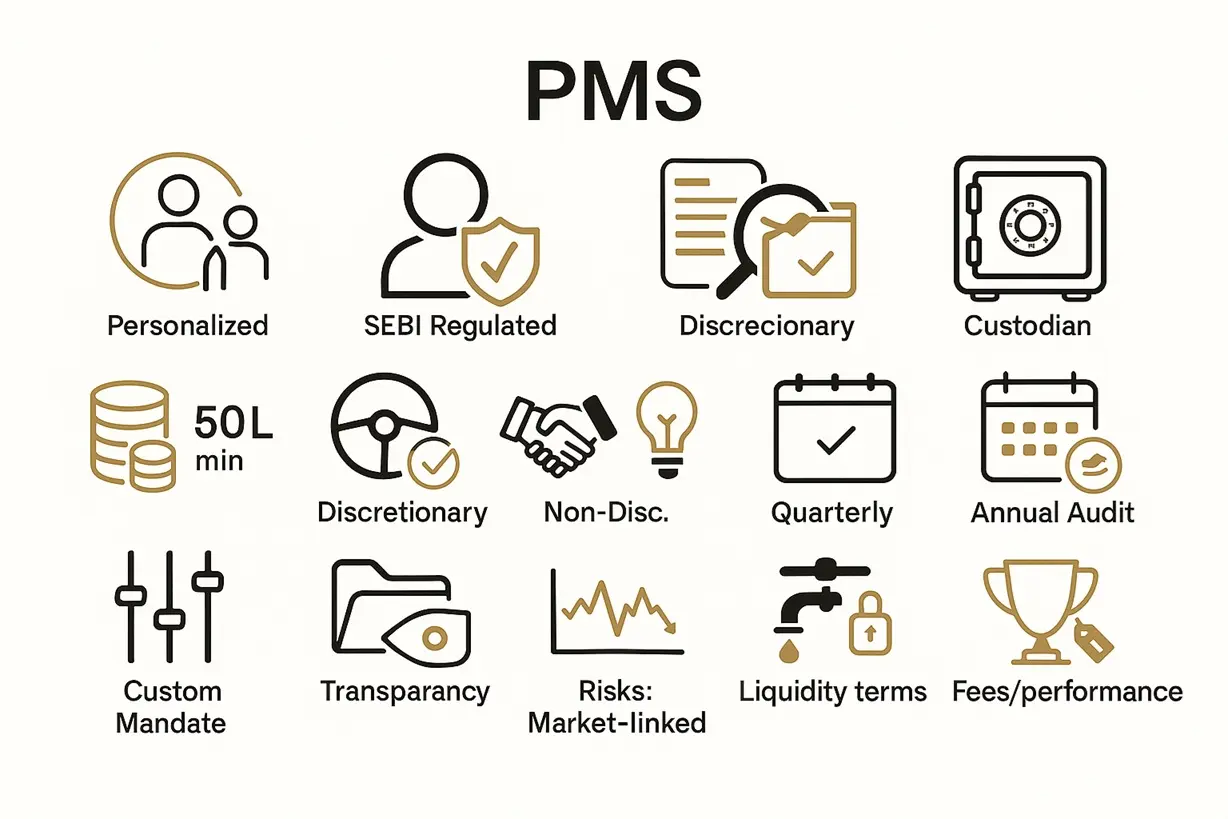

For HNIs who want a personalised portfolio—not a pooled product—Portfolio Management Services (PMS) offer tailored strategies managed by SEBI-registered professionals, with holdings maintained in the client’s own demat/custody setup and periodic reporting under a consolidated SEBI framework.

What is Portfolio Management Services (PMS)

Portfolio Management Services (PMS) are managed accounts where a SEBI-registered Portfolio Manager constructs and runs an investment portfolio for an individual client (or eligible entity). PMS operates under a single, consolidated regulatory framework (SEBI’s Master Circular for Portfolio Managers). Securities and Exchange Board of India

Minimum investment: ₹50 lakh (current SEBI requirement).

Account & custody: PMS providers open/maintain a dedicated PMS + demat arrangement mapped to a SEBI-registered custodian; securities/funds are settled and reported specifically for each client. apmiindia.org

Periodic reporting: Clients receive quarterly statements and an audited annual account statement, as prescribed.

Types of PMS

Discretionary: The portfolio manager takes buy/sell decisions on your behalf in line with your stated objectives. apmiindia.org

Non-Discretionary: The manager recommends; you approve before execution. apmiindia.org

Advisory: Pure advice; execution and custody remain with you.

Why PMS? (Key Benefits for HNIs)

Deep Customisation: Mandates can reflect your risk profile, cash-flow needs, sector preferences, exclusions (“negative lists”), and tax constraints, instead of a one-size-fits-all pool. apmiindia.org

Transparency & Control: You see underlying securities via your own demat/custody mapping and receive formal periodic statements. apmiindia.org

Professional Management: Managed by SEBI-registered portfolio managers under a codified rulebook and disclosures. Securities and Exchange Board of India

Risks to Understand

PMS is market-linked. Returns can be volatile, and there are no guarantees. Liquidity depends on the underlying holdings and the terms in your PMS agreement. Fees and performance-fee constructs (if any) vary by provider; review all disclosures, risks, and costs in the PMS Disclosure Document before investing. (SEBI prescribes what’s disclosed and how often.)

Who should consider PMS? (Key Takeaway)

If you have ₹50 lakh+ to allocate, want bespoke portfolio construction, prefer direct visibility into holdings, and value professional oversight within a SEBI-regulated framework, PMS can be a strong fit.

________________________________________

Disclaimer

This blog is for educational purposes only and does not constitute investment advice. Past performance may or may not be sustained in the future. Investments in AIFs and PMS are subject to market risks. Please consult your SEBI-registered investment adviser before investing.